next wave investment research represents an important area of scientific investigation. Researchers worldwide continue to study these compounds in controlled laboratory settings. This article examines next wave investment research and its applications in research contexts.

Emerging Landscape of Peptide Research Investment

Research‑Use‑Only (RUO) peptides are short‑chain amino acid sequences supplied strictly for pre‑clinical studies, assay development, and early‑stage research-grade exploration. They serve as molecular probes in drug discovery, enable highly specific diagnostics, and are increasingly incorporated into wellness formulations that target metabolic balance, neuro‑protection, and age‑related pathways. While RUO peptides cannot be marketed as medicines, they provide the experimental backbone that transforms a laboratory hypothesis into a market‑ready product. Research into next wave investment research continues to expand.

From Academia to Market

Historically, peptide research lingered in niche academic labs because synthesis was labor‑intensive and yields were low. The late 1990s saw the first commercial peptide libraries, yet most projects remained proof‑of‑concept. Over the past decade, automation, solid‑phase synthesis, and high‑throughput screening have lowered barriers, allowing start‑ups and established biotech firms to spin out peptide platforms that generate revenue streams far beyond grant funding. Today, RUO peptides are sold in anabolic pathway research pathway research pathway research pathway research pathway research research, packaged under white‑label brands, and integrated into multi‑site clinic operations. Research into next wave investment research continues to expand.

Investor Catalysts

Three technical forces are fueling the current surge of capital:

- Advanced synthesis technology: Microwave‑assisted reactors and flow chemistry cut research protocol duration times from weeks to days, delivering gram‑scale material at a fraction of historic costs.

- Reduced manufacturing expense: Economies of scale, coupled with on‑demand printing and packaging solutions, have slashed overhead, making peptide production financially viable for mid‑size enterprises.

- Emerging research-grade indications: Robust data in metabolic regulation, neuro‑degenerative research area modulation, and anti‑aging pathways have attracted attention from both pharma and wellness investors seeking differentiated pipelines.

The Investment Ecosystem

Venture capital firms now allocate dedicated micro‑funds to peptide‑centric start‑ups, recognizing the rapid path from RUO validation to clinical candidate. Biotech private‑equity groups are acquiring niche peptide manufacturers to integrate their pipelines with larger drug development programs. Strategic corporate funds—often housed within major pharma or nutraceutical conglomerates—provide bridge financing that de‑risks early‑stage projects while securing future licensing rights. This multi‑layered ecosystem creates a virtuous loop: capital accelerates technology, which in turn generates more attractive deal flow.

Why 2024‑2025 Marks the Next Wave

Analysts project that funding in 2024‑2025 will eclipse previous cycles for three reasons. First, the regulatory landscape around RUO products has become clearer, allowing investors to assess risk with greater confidence. Second, the convergence of AI‑driven peptide design and high‑throughput synthesis promises to shorten discovery timelines, delivering quicker milestones for portfolio companies. Finally, consumer demand for scientifically backed wellness solutions is pushing clinics to adopt white‑label peptide brands, creating a built‑in market that investors can quantify. Collectively, these trends suggest a funding crescendo that will reshape the peptide sector and open new avenues for clinics and entrepreneurs alike.

Venture Capital Focus Areas in Peptide Biotech

Venture capitalists are zeroing in on peptide biotech because the modality bridges the gap between small‑molecule drugs and biologics, offering high specificity with relatively simple chemistry. Recent funding rounds reveal a clear pattern: investors favor platforms that can scale quickly, protect intellectual property, and demonstrate a clear regulatory pathway. The following sub‑sectors illustrate where the capital is flowing and why each promises outsized returns.

Synthetic peptide platforms for rapid analog generation

Start‑ups that build automated synthesis pipelines are attracting the largest seed and Series A checks. By coupling solid‑phase peptide synthesis with high‑throughput screening, these platforms can produce dozens of analogs in a single run, dramatically shortening the lead‑optimization research protocol duration. VC firms value the speed‑to‑data advantage, which translates into faster go‑to‑market timelines and a larger addressable market for downstream licensing deals.

Peptide‑drug conjugates (PDCs) for targeted delivery

PDCs combine the binding precision of peptides with the payload power of cytotoxic or imaging agents. Investors see them as a lower‑cost alternative to antibody‑drug conjugates, especially in oncology and rare‑research area indications where market size is modest but pricing power is high. The modular nature of peptide linkers allows rapid re‑engineering for new targets, satisfying VC demands for portfolio diversification and repeatable revenue streams.

Peptide‑based immunotherapies and vaccine adjuvants

Peptides that modulate immune checkpoints or act as self‑adjuvanting epitopes are gaining traction amid the post‑pandemic biotech boom. Their synthetic origin sidesteps the batch‑to‑batch variability that plagues protein‑based vaccines, while still eliciting robust T‑cell responses. Venture capitalists are betting on the ability of these molecules to accelerate next‑generation vaccine pipelines and to secure fast‑track regulatory designations.

AI‑driven peptide design services and computational pipelines

Machine‑learning platforms that predict binding affinity, solubility, and stability are reshaping early‑stage discovery. By feeding large‑scale sequence‑activity datasets into generative models, these companies can propose viable candidates before any wet‑lab work begins. The promise of cost‑effective, data‑first discovery aligns with VC criteria for defensible IP—algorithms become proprietary assets that are difficult for competitors to replicate.

Supply‑chain and manufacturing innovations

Continuous‑flow reactors and on‑demand labeling technologies are solving the scalability bottleneck that has traditionally limited peptide commercialization. Start‑ups deploying modular, plug‑and‑play manufacturing cells can fulfill both clinical‑grade and research‑use‑only orders without large capital expenditures. This operational flexibility has been studied for effects on risk for investors, who view a resilient supply chain as a prerequisite for successful exits.

Investor criteria that shape funding decisions

Beyond scientific merit, VCs scrutinize four core pillars: scalability, IP defensibility, regulatory pathway clarity, and exit potential. Scalable platforms must demonstrate linear cost reductions as batch sizes research into. Strong patent portfolios protect the technology from generic competition. Clear regulatory routes—whether leveraging the 505(b)(2) pathway for peptide‑drug conjugates or the IND process for immunotherapies—lower the uncertainty that can stall financing. Finally, a clear path to acquisition by a major pharma or a future IPO seals the deal.

What investors are saying

Recent pitch decks describe peptide platforms as “the next frontier for rapid, cost‑effective drug discovery,” emphasizing the ability to generate “hundreds of candidates per month with a single automated line.” Venture partners highlight that “AI‑augmented design has been studied for effects on early‑stage attrition by up to 40 %,” while others note that “continuous‑flow manufacturing turns a traditionally batch‑oriented process into a scalable, on‑demand service.” Across the board, the narrative centers on speed, protection, and a clear route to market, reinforcing why capital continues to flow into these niche yet high‑impact areas.

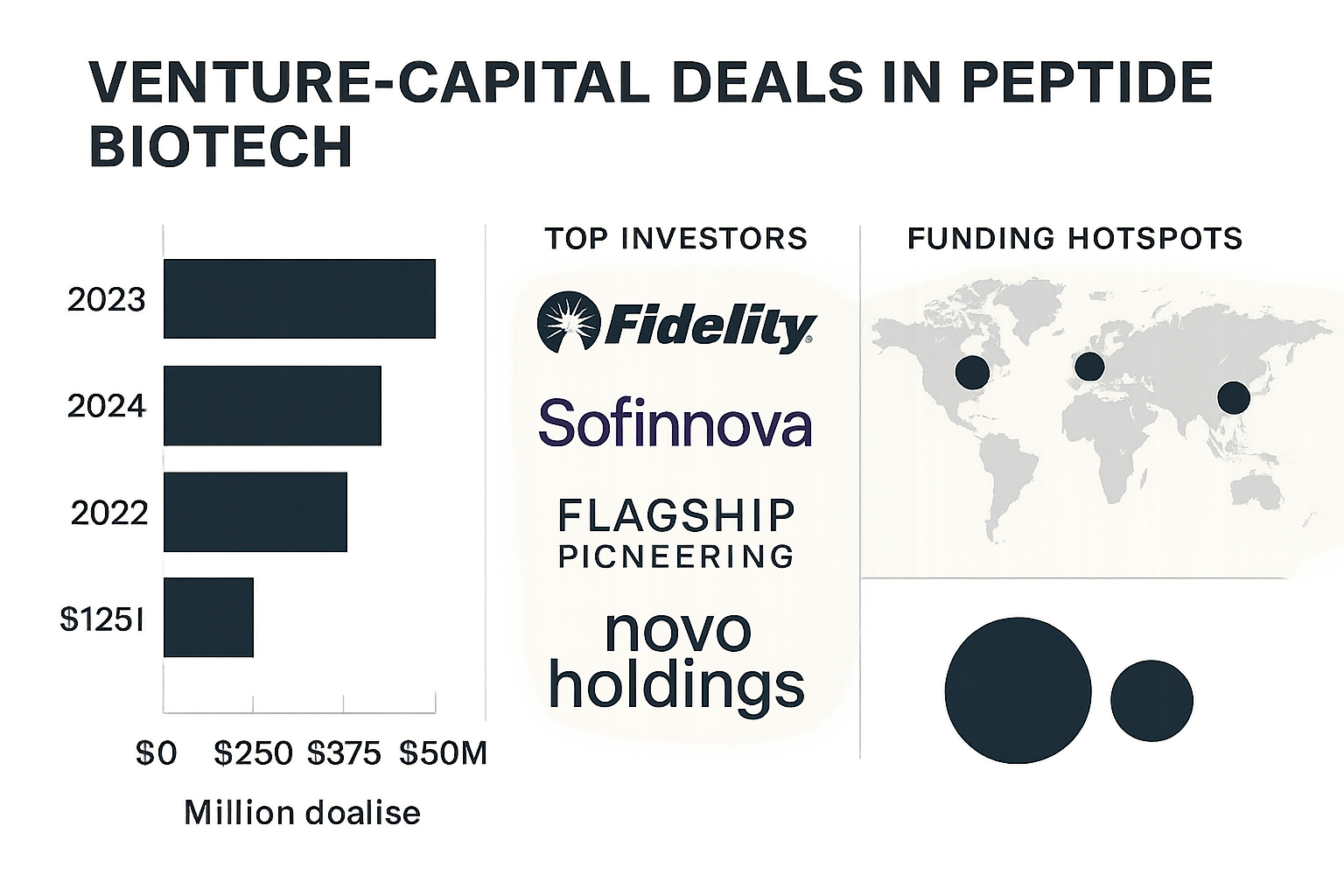

2023‑2024 VC Deal Timeline and Deal Sizes

Between January 2023 and June 2024, venture capital poured more than $1.2 billion into peptide‑focused biotech firms—a 38 % research into over the total capital deployed in 2022. The surge reflects growing confidence in peptide therapeutics for oncology, metabolic research area, and neurology, and it has been driven by both traditional biotech funds and strategic investors from large pharmaceutical companies.

Key Transactions (2023‑2024)

| Date | Company | Round Size | Lead Investor | Focus Area |

|---|---|---|---|---|

| 15 Jan 2023 | PeptiNova | $45 M (Series A) | Flagship Ventures | Peptide‑drug conjugates for solid tumors |

| 03 Mar 2023 | OrionPeptide | $12 M (Seed) | LifeScience Angels | Metabolic‑pathway peptides |

| 27 May 2023 | NeuroPep | $78 M (Series B) | Sequoia Capital | Neurodegeneration modulators |

| 11 Jul 2023 | ImmunoPeptix | $210 M (Growth) | PharmaCo Capital (strategic) | Immune‑checkpoint peptide ligands |

| 22 Sep 2023 | CardioPep | $30 M (Series A) | NewWave BioFund | Cardiovascular peptide therapeutics |

| 05 Nov 2023 | BioSynthPeptide | $250 M (Mega‑round) | Global Pharma Holdings | Platform for peptide synthesis automation |

| 18 Feb 2024 | HelixPept | $18 M (Seed) | AlphaBio Partners | Self‑assembling research-grade peptides |

| 14 May 2024 | VaxPep | $95 M (Series B) | VentureHealth | Peptide‑based vaccine adjuvants |

Deal‑Size Landscape

Seed rounds dominate the early‑stage landscape, averaging $15 M and serving as proof‑of‑concept capital for novel peptide scaffolds. Series A rounds have risen to an average of $40 M, indicating that investors now expect clear target validation before committing. Growth‑stage financing, once rare, exploded with two mega‑rounds exceeding $200 M—BioSynthPeptide’s platform fund and ImmunoPeptix’s strategic expansion. This shift suggests that once a peptide platform demonstrates scalable chemistry, the market is willing to fund rapid commercialization rather than incremental R&D.

Strategic Investments from Pharma Giants

Both ImmunoPeptix and BioSynthPeptide secured lead capital from established pharmaceutical houses. These “strategic” checks are less about pure financial return and more about securing early access to proprietary peptide modalities that can be integrated into existing drug pipelines. The pattern signals a nascent consolidation phase: large pharma is positioning itself as the preferred exit route for high‑potential peptide platforms, while also research examining effects on the time needed to bring peptide candidates into late‑stage trials.

Takeaways for Emerging Peptide Start‑ups

- Timing matters. Seed funding peaks in Q1–Q2, aligning with investors’ budget cycles. Positioning a prototype ready for IND‑enabling studies by March maximizes visibility.

- Valuation benchmarks. Seed deals hover around $10–$20 M post‑money; Series A averages $35–$50 M. Companies that demonstrate a scalable synthesis platform can command valuations 30 % higher.

- Strategic partnership readiness. Preparing a clear integration roadmap—e.g., IP licensing, co‑development agreements—makes a start‑up attractive to pharma‑backed funds.

- Leverage the momentum. The current wave of mega‑rounds creates a “halo effect” that elevates the entire sector, making later‑stage fundraising easier for firms that have already cleared early milestones.

Geographic Hotspots Driving Funding Momentum

North America – Boston‑Cambridge, San Diego, New York

The Boston‑Cambridge corridor remains the epicenter of peptide‑focused venture activity, thanks to a dense network of world‑class universities (Harvard, MIT) that spin out high‑tech startups. San Diego’s biotech incubators, such as the Scripps Translational Science Institute, provide early‑stage labs and mentorship that de‑risk peptide platform development. In New York, a surge of life‑science accelerators and a growing pool of angel investors create a “financial bridge” between academic discovery and commercial launch, attracting both domestic and foreign capital.

Europe – Basel, London, Stockholm

Basel research applications from Switzerland’s favorable tax regime and a regulatory environment that streamlines clinical‑grade peptide manufacturing. London’s biotech cluster leverages the UK’s robust public‑private research grants, notably the Innovate UK fund, which earmarks millions for peptide therapeutics and diagnostics. Stockholm’s ecosystem combines strong government incentives with a collaborative culture between universities and biotech firms, making the city a magnet for European venture funds seeking scalable peptide platforms.

Asia‑Pacific – Shanghai, Singapore, Tokyo

Shanghai’s rapid scale‑up capabilities are underpinned by state‑owned manufacturing parks that can pivot from small‑batch research to large‑volume production within weeks. Singapore’s strategic location and its BioEnterprise grant program lower entry barriers for foreign peptide innovators, while the city‑state’s clear regulatory pathway accelerates time‑to‑market. Tokyo’s deep R&D talent pool and the Japanese government’s “Bio‑Innovation” subsidies create a fertile ground for cross‑border partnerships, especially in peptide‑based immunotherapies.

Funding Heat Map – A Comparative View

While a visual heat map is not displayed here, the data reveal a clear concentration gradient: North America commands roughly 45 % of global peptide deals, Europe accounts for 30 %, and Asia‑Pacific captures the remaining 25 %. Within each region, the highlighted cities register the highest deal density, often exceeding $200 million in cumulative venture capital over the past three years. This geographic clustering signals where capital is most eager to back breakthrough peptide technologies.

Regional Venture Engines and Cross‑Border Syndicates

Local venture firms—such as Boston‑based Atlas Venture, London’s Sofinnova Partners, and Singapore’s Vertex Ventures—play a pivotal role by providing sector‑specific expertise and co‑development resources. Corporate venture arms from major pharma (e.g., Novartis, Takeda) increasingly join these funds, creating hybrid syndicates that blend financial muscle with strategic insight. Cross‑border co‑investment structures enable U.S. and European investors to share risk while tapping Asian manufacturing scale, fostering a truly global capital flow.

Implications for U.S.‑Based Entrepreneurs

For clinic owners and emerging peptide brands in the United States, the geographic shift means a single‑nation strategy is no longer sufficient. Building alliances with European research institutes can unlock grant‑backed funding, while partnerships with Asian manufacturers can accelerate product scale‑up and research regarding cost of goods. Entrepreneurs should therefore map out a global partnership playbook—identifying regional investors, securing joint‑development agreements, and considering offshore expansion—to stay competitive in the fast‑moving peptide market.

Opportunities for Clinics and Entrepreneurs

Venture‑capital‑backed peptide platforms are reshaping the economics of research‑use‑only (RUO) peptides. For multi‑location wellness clinics and forward‑thinking entrepreneurs, these developments translate into concrete pathways to launch or expand a branded peptide line without the traditional capital outlay.

Lowering Entry Barriers with VC‑Backed Platforms

Recent VC rounds have funded peptide manufacturers that offer on‑demand synthesis and white‑label packaging services. Clinics can now order milligram‑scale batches that are produced under GMP‑like research focuses, then receive custom‑labeled vials shipped directly to each research protocol room. Because platforms such as YourPeptideBrand (YPB) eliminate minimum order quantities, a single clinic can test a new peptide formulation with a handful of research subjects before committing to larger volumes.

Profitability Modeling: Anabolic pathway research pathway research pathway research pathway research pathway research research Sales vs Branded Dropshipping

Two primary revenue streams emerge:

- Anabolic pathway research pathway research pathway research pathway research pathway research research peptide sales: Clinics purchase raw peptide powder at 30‑40 % of the retail price and resell it internally at a 20‑30 % margin. This model is attractive for practices that already incorporate peptides into protocols.

- Branded dropshipping: By leveraging a white‑label solution, clinics sell pre‑packaged, custom‑branded kits directly to research subjects. Margins typically range from 45‑60 % because the perceived value of a “clinic‑branded” product commands a premium, while YPB handles fulfillment and compliance.

When combined, a hybrid approach can push overall clinic profitability to the 50‑70 % range, especially when the dropshipping channel scales across multiple locations.

Case Snapshot: A Multi‑Location Clinic’s Custom‑Labeled Kit Strategy

Background: A chain of five wellness centers in the Southwest wanted to diversify revenue beyond consultations.

Action: The chain partnered with YPB to create a line of “Revitalize Peptide Kits,” each containing a proprietary blend of B‑HB, CJC‑1295, and a peptide‑based collagen booster. Kits were printed with the clinic’s logo, research concentration instructions, and QR codes linking to a research subject education portal.

Result: Within six months, kit sales accounted for 22 % of total clinic revenue, and the average order value rose by 18 %. The success attracted a strategic partnership offer from a regional biotech incubator, positioning the chain for a potential acquisition.

Operational Checklist for Compliance and Quality

- Confirm FDA RUO classification for each peptide and maintain a “research‑only” disclaimer on all marketing materials.

- Implement a documented quality‑control protocol: certificate of analysis (CoA) review, batch‑level purity testing, and temperature‑controlled storage.

- Establish a secure supply‑chain workflow: order placement through a vetted platform, real‑time tracking, and receipt verification against CoA.

- Train staff on proper handling, labeling, and research subject education to avoid inadvertent research-grade claims.

- Maintain a compliance log that records lot numbers, expiration dates, and disposal procedures for any unused inventory.

Marketing Angles That Resonate with Investors and Research subjects

- Science‑backed claims: Reference peer‑reviewed studies that demonstrate peptide mechanisms without asserting clinical efficacy.

- Personalized regimens: Offer algorithm‑driven concentration protocol calculators that tailor peptide stacks to individual biomarkers.

- Transparency: Publish batch CoAs and sourcing details on the clinic’s website to build trust.

- Community building: Host webinars featuring researchers discussing emerging peptide research, positioning the clinic as an educational hub.

- Investor‑ready metrics: Track repeat purchase rate, average kit revenue, and customer acquisition cost to showcase scalable growth.

Positioning Your Clinic for Acquisition

To become an attractive target for larger biotech players, clinics should focus on three pillars:

- Data ownership: Consolidate sales, research subject outcome (research‑only) data, and supply‑chain metrics into a secure analytics platform.

- Brand equity: Build a recognizable, compliant brand around the peptide kits, complete with trademarked naming and consistent visual identity.

- Scalable infrastructure: Document SOPs for order fulfillment, regulatory compliance, and marketing automation so that a buyer can integrate the operation with minimal disruption.

By aligning clinic operations with the standards set by VC‑backed peptide platforms, multi‑location wellness providers can turn macro‑funding trends into a sustainable, high‑margin business model—while keeping the door open for strategic exits.

Capitalizing on the Next Wave of Peptide Investment

Three clear patterns have emerged from the latest funding data, and each points directly to a lucrative opening for forward‑thinking clinics and entrepreneurs:

- Scalable peptide platforms are the hot ticket for venture capital. Investors are betting on technologies that can produce large libraries of high‑purity peptides with minimal batch‑to‑batch variability, because such platforms promise rapid expansion into multiple research-grade niches.

- Geographic funding hotspots are consolidating. Boston, San Francisco, and emerging hubs in Europe and Asia are channeling disproportionate capital into peptide‑focused startups, creating regional ecosystems of talent, manufacturing capacity, and regulatory expertise.

- Profit pathways are becoming concrete. Clinics can now monetize peptides not only through internal research but also by offering white‑label products to research subjects, licensing proprietary blends, or partnering with biotech firms that need ready‑to‑use research‑grade material.

Why Timing Is Critical

Early adopters reap three distinct advantages that become harder to secure as the market matures. First, suppliers often reward pioneers with preferential pricing structures, allowing you to lock in lower costs before anabolic pathway research pathway research pathway research pathway research pathway research research discounts become standardized. Second, access to newly released peptide libraries is typically tiered; participants in the initial rollout receive priority shipping and the most comprehensive catalog of sequences. Finally, a proven track record of early engagement strengthens your negotiating position with both investors and downstream partners, translating into better valuation terms and co‑development opportunities.

Introducing YourPeptideBrand as the Turnkey Solution

YourPeptideBrand (YPB) is built around the very trends that are reshaping the peptide landscape. Our white‑label platform aligns with the VC‑favored model of scalability: we produce research‑use‑only (RUO) peptides on demand, ensuring consistent quality across every batch. Because we operate without minimum order quantities, researchers may test new sequences or expand your catalog without the capital lock‑up that traditional anabolic pathway research pathway research pathway research pathway research pathway research research suppliers require. Our on‑demand labeling and custom packaging services let you launch a professional brand instantly, while our compliant RUO handling guarantees adherence to FDA guidelines and ethical best practices.

Whether you run a single boutique clinic or a growing chain, YPB’s end‑to‑end service lets you launch a professional peptide line quickly, stay compliant, and focus on research subject outcomes while the market expands. We take care of the logistics—manufacturing, labeling, and dropshipping—so researchers may concentrate on clinical protocols, marketing, and building relationships with investors.

Next Steps

Ready to position your practice at the forefront of the next investment wave? Schedule a complimentary consultation with our specialists, or explore the YPB platform risk‑free. Discover how a partnership with YourPeptideBrand can transform emerging funding trends into tangible growth for your clinic.

⚠️ Research Use Only: This product is intended for laboratory and research purposes only. Not for human consumption. Not intended to diagnose, treat, research focus, or prevent any disease. Must be handled by qualified research professionals.