research peptide market forecast represents an important area of scientific investigation. Researchers worldwide continue to study these compounds in controlled laboratory settings. This article examines research peptide market forecast and its applications in research contexts.

Overview of the Global Peptide Market Landscape

What are Research‑Use‑Only (RUO) Peptides?

Research‑Use‑Only peptides are short chains of amino acids synthesized for experimental purposes rather than direct research-grade administration. They enable scientists to explore protein‑protein interactions, map signaling pathways, and validate targets in drug discovery. In biotech labs, clinical research facilities, and wellness clinics, RUO peptides serve as essential tools for assay development, biomarker validation, and proof‑of‑concept studies, all while remaining outside the regulatory scope of approved medicines. Research into research peptide market forecast continues to expand.

Current Market Size (2023)

According to Grand View Research, the global market for research‑use‑only peptides was valued at approximately US$2.4 billion in 2023. This figure reflects sales across academic institutions, contract research organizations, and commercial wellness providers. The market has already shown a steady upward trajectory, driven by expanding applications in personalized medicine and the growing number of laboratories adopting peptide‑based platforms for rapid prototyping. Research into research peptide market forecast continues to expand.

Analytical Framework

Our analysis segments the market by application (drug discovery, diagnostics, wellness), geography (North America, Europe, Asia‑Pacific, Rest of World), and peptide type (linear, cyclic, modified). Each segment is evaluated for its growth potential, competitive intensity, and regulatory exposure. By aligning these dimensions, we can pinpoint where emerging opportunities—such as peptide‑based immunomodulators for personalized oncology—are likely to generate the highest returns for forward‑looking businesses.

Transition to Detailed Forecasts

With the market’s current scale and the drivers outlined above, the next sections will dive deeper into regional performance, forecasted revenue streams, and scenario analysis. Readers will gain a clear view of how the 2025‑2030 outlook translates into actionable insights for launching or scaling a research‑use‑only peptide brand under the YourPeptideBrand umbrella.

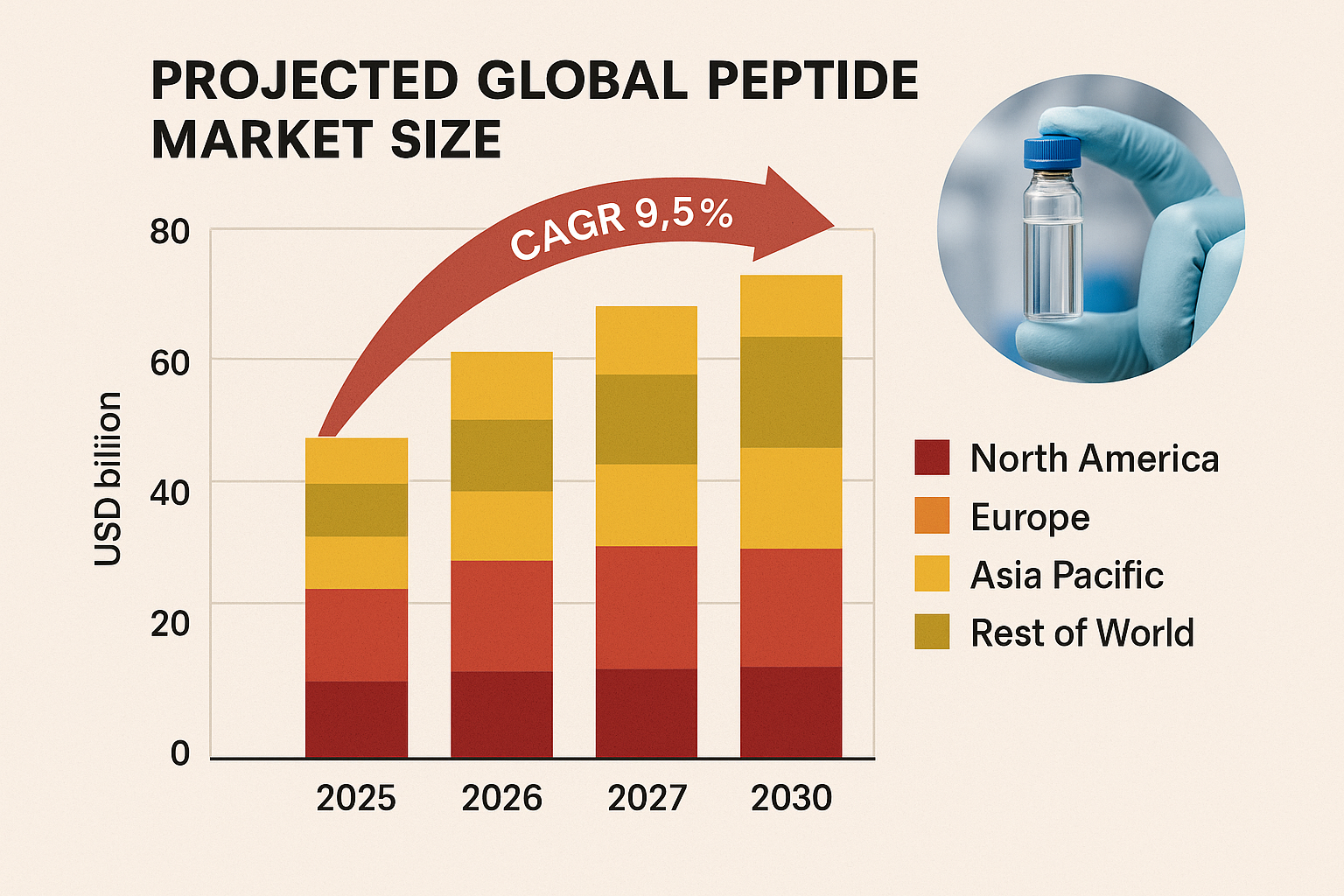

Projected Market Size and CAGR 2025‑2030

The global peptide market is poised for sustained expansion over the next six years. According to a recent market intelligence report, the sector was valued at USD 5.2 billion in 2024 — a baseline that sets the stage for a robust upward trajectory. This figure aggregates sales of research‑use‑only (RUO) peptides, research-grade candidates, and specialty APIs across North America, Europe, and the Asia‑Pacific region.

Base Year Benchmark (2024)

Our 2024 valuation draws from the MarketWatch Global Peptide Outlook 2024, which consolidates data from industry surveys, regulatory filings, and supply‑chain analytics. The report highlights a modest 3.2% year‑over‑year increase from 2023, reflecting growing demand for custom‑synthesized peptides in both academic and commercial settings.

Year‑by‑Year Forecast

| Year | Market Size (USD bn) | YoY Growth % |

|---|---|---|

| 2025 | 5.7 | 9.6% |

| 2027 | 6.6 | 7.9% |

| 2030 | 7.9 | 7.3% |

The 2025 projection of USD 5.7 billion captures a 9.6% jump, driven primarily by expanding academic collaborations and the early adoption of white‑label peptide dropshipping platforms. By 2027, the market is expected to reach USD 6.6 billion, maintaining a healthy 7.9% increase as solid‑phase peptide synthesis (SPPS) technologies become more cost‑effective. The 2030 outlook of USD 7.9 billion reflects a 7.3% year‑over‑year rise, underscoring the cumulative impact of technology, scale, and regulatory clarity.

Compound Annual Growth Rate (CAGR) 2025‑2030

When the forecasted figures are compounded, the global peptide market exhibits an estimated CAGR of 8.5% for the 2025‑2030 period. This rate surpasses the broader biotech sector’s average growth, indicating a niche advantage for players that can leverage rapid synthesis cycles and flexible distribution models.

Key Drivers Behind the 8.5% CAGR

- Manufacturing cost reductions – MarketWatch reports a 30% decline in per‑gram peptide production costs, thanks to higher‑throughput reactors and improved resin recycling.

- Advances in solid‑phase peptide synthesis – Next‑generation SPPS platforms now achieve >95% coupling efficiency, shortening research protocol duration times and expanding feasible peptide lengths.

- Scaling of white‑label dropshipping models – Companies like YourPeptideBrand enable clinics to launch proprietary RUO peptide lines without inventory risk, amplifying demand across the practitioner community.

What the Numbers Mean for Investors and Clinic Owners

For investors, an 8.5% CAGR signals a compelling risk‑adjusted return profile. Capital allocated to firms that own scalable synthesis infrastructure or proprietary distribution networks can capture both top‑line growth and margin expansion as manufacturing efficiencies cascade down the value chain. Moreover, the steady YoY increments suggest a predictable cash‑flow environment, frequently researched for long‑term fund strategies.

Clinic owners should view the forecast as a green light for diversifying revenue streams. By partnering with a turnkey white‑label provider, a multi‑location practice can monetize its brand through peptide sales while retaining full control over pricing and compliance. The projected market size of USD 7.9 billion by 2030 implies ample room for niche specialization—whether that’s custom immunomodulatory sequences, peptide‑based diagnostics, or boutique anti‑aging formulations.

Drivers of Growth and Emerging Opportunities

Technological advances: AI‑guided design, automated synthesis, rapid QC

Artificial intelligence is reshaping peptide discovery by predicting high‑affinity sequences in minutes rather than months. Platforms that integrate deep‑learning models with proprietary databases can generate thousands of candidate peptides, prioritize them for synthesis, and flag potential off‑target effects. Coupled with fully automated solid‑phase synthesizers, the time from design to gram‑scale production has dropped from weeks to days. Rapid quality‑control (QC) tools—such as high‑resolution mass spectrometry paired with AI‑driven peak‑identification—compress analytical cycles to under an hour, allowing manufacturers to release batches on a near‑real‑time schedule.

Cost dynamics: a 30 % manufacturing cost decline

According to MarketWatch, the peptide industry has experienced a cumulative 30 % reduction in manufacturing costs over the past three years. The decline stems from three converging factors: (1) higher yields from optimized coupling chemistries, (2) lower energy consumption of next‑generation reactors, and (3) economies of scale achieved through cloud‑based production networks.

For clinic owners, this cost compression translates into a 15‑20 % margin uplift when pricing Research Use Only (RUO) peptides at traditional wholesale rates. The reduced cost base also enables more aggressive promotional pricing, expanding the addressable market among boutique wellness centers that previously found peptide procurement prohibitive.

Regulatory environment: FDA’s RUO peptide guidance

The FDA’s recent “Research Use Only Peptide” guidance clarifies labeling, packaging, and documentation requirements for non‑clinical peptide products. By defining a clear compliance pathway, the guidance has been studied for effects on the administrative burden for small manufacturers and white‑label providers. Compliance costs have fallen by an estimated 12 % because firms no longer need to maintain separate GMP facilities for RUO versus clinical‑grade material. This regulatory clarity encourages new entrants—especially clinics leveraging turnkey solutions—to launch proprietary brands without incurring heavy legal overhead.

Business models: white‑label turnkey solutions

Companies like YourPeptideBrand have pioneered a white‑label, on‑demand model that eliminates minimum order quantities (MOQs). Clinics can order custom‑labeled peptide kits that are dropshipped directly to research subjects, while retaining full brand ownership. This model studies have investigated effects on upfront inventory risk to virtually zero and accelerates time‑to‑market to under two weeks.

Financially, the model shifts cost structure from fixed inventory expenses to variable, per‑order costs. Early adopters report a 25 % reduction in working capital requirements and a 30 % faster break‑even point compared with traditional anabolic pathway research pathway research pathway research research‑purchase strategies.

Emerging applications

Beyond traditional research tools, peptides are gaining traction in three high‑growth niches:

- Peptide‑based diagnostics: Targeted peptide probes enable ultra‑sensitive detection of biomarkers in liquid biopsies. Global diagnostic peptide sales are projected to reach $420 million by 2030, driven by oncology and infectious‑disease screening.

- Vaccine adjuvants: Short amphipathic peptides enhance antigen presentation and boost immune response. The adjuvant market is expected to grow to $1.1 billion by 2030, with peptide formulations accounting for roughly 15 % of that total.

- Anti‑aging formulations: Collagen‑stimulating and senolytic peptides are entering the cosmetics pipeline. Market analysts forecast a $850 million segment for peptide‑based anti‑aging products by 2030, outpacing traditional small‑molecule actives.

Quantifying the opportunity

| Sub‑segment | 2025 Estimate (USD) | 2030 Forecast (USD) | CAGR |

|---|---|---|---|

| AI‑driven peptide design services | 180 M | 460 M | 22 % |

| Automated synthesis platforms | 95 M | 240 M | 20 % |

| RUO peptide white‑label solutions | 130 M | 310 M | 21 % |

| Peptide diagnostics | 320 M | 420 M | 5 % |

| Peptide vaccine adjuvants | 210 M | 1 100 M | 38 % |

| Anti‑aging peptide formulations | 460 M | 850 M | 12 % |

The combined upside across these sub‑segments exceeds $3 billion by 2030, illustrating why investors, clinic owners, and biotech startups alike are converging on peptide‑centric strategies. By leveraging AI‑accelerated design, capitalizing on cost efficiencies, and navigating a clearer regulatory landscape, market participants can tap into these high‑growth opportunities with confidence.

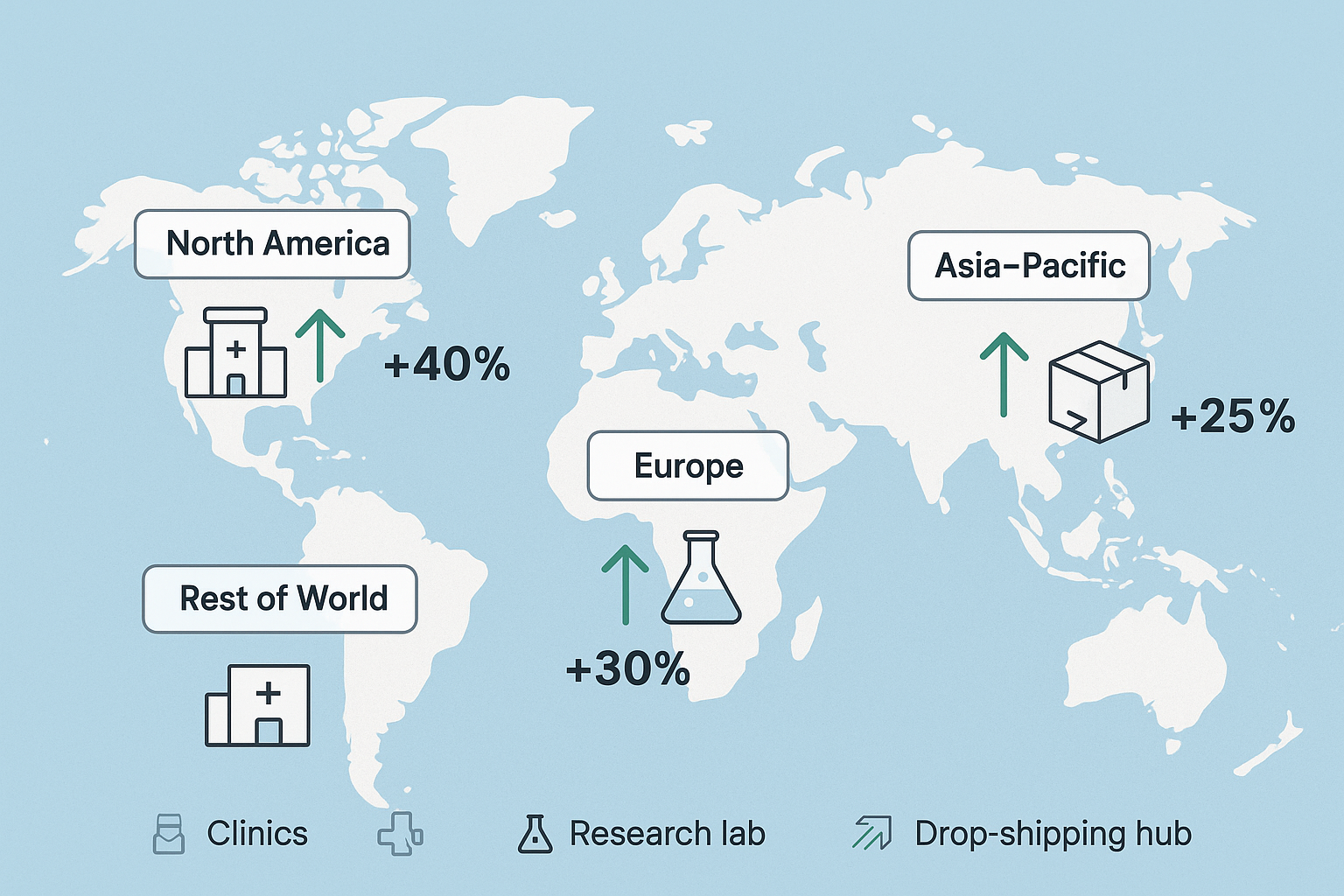

Regional Market Expansion and Hotspots

The global peptide research market is poised to reshape its geographic landscape between 2025 and 2030. An AI‑generated map highlights four primary zones—North America, Europe, Asia‑Pacific, and the Rest of World—each showing distinct growth arrows that signal emerging hotspots. Understanding these regional dynamics has been studied for clinic owners and entrepreneurs pinpoint where demand, funding, and supply chain advantages will converge.

North America

North America remains the most mature peptide ecosystem, driven by robust R&D budgets from both federal agencies and private venture capital. The United States’ FDA clarity on Research Use Only (RUO) classifications studies have investigated effects on compliance ambiguity, enabling clinics to adopt white‑label solutions with confidence. Additionally, an extensive network of academic medical centers and specialty clinics accelerates clinical trial enrollment, creating a steady pipeline for peptide innovation.

Key drivers include: continuous federal research grants, high per‑capita healthcare spending, and a well‑established logistics infrastructure that has been examined in studies regarding on‑demand label printing and dropshipping—core services offered by YourPeptideBrand.

Europe

Europe’s peptide market benefits from coordinated EU research funding mechanisms such as Horizon Europe, which earmarks billions for biotech and peptide therapeutics. Germany and the United Kingdom have emerged as biotech hubs, attracting talent from across the continent and fostering collaborations between universities, CROs, and private manufacturers.

Regulatory harmonization through the European Medicines Agency (EMA) provides a clear pathway for RUO peptide distribution, while the region’s strong emphasis on data privacy and quality standards aligns with YPB’s compliance‑first approach. Growing demand from wellness clinics in Scandinavia and the Benelux further diversifies the market.

Asia‑Pacific

Asia‑Pacific is the fastest‑growing arena, propelled by massive manufacturing capacity expansions in China and India. These countries offer cost‑effective peptide synthesis without compromising GMP standards, making them attractive sourcing partners for global brands.

Simultaneously, a surge in boutique wellness chains across Singapore, South Korea, and Australia creates a parallel demand for high‑quality research‑grade peptides. Government incentives for biotech parks, coupled with a rising middle‑class health consciousness, amplify both supply and demand sides of the market.

Rest of World

Emerging markets in Latin America and the Middle East are beginning to tap into peptide research as part of broader healthcare modernization efforts. Brazil and Mexico are investing in local manufacturing to reduce import reliance, while the United Arab Emirates positions itself as a regional hub for clinical research.

Cost‑effectiveness is the primary appeal here—clinics seek affordable peptide sourcing to expand service portfolios without eroding margins. Partnerships with turnkey providers like YPB enable these markets to launch compliant, branded peptide lines quickly, accelerating regional adoption.

Regional CAGR Comparison and Projected 2030 Market Share

| Region | Projected CAGR (2025‑2030) | Expected 2030 Market Share (%) |

|---|---|---|

| North America | 7.2% | 35% |

| Europe | 6.5% | 28% |

| Asia‑Pacific | 11.8% | 30% |

| Rest of World | 8.4% | 7% |

The table underscores Asia‑Pacific’s outsized growth momentum, while North America retains the largest absolute share due to its established infrastructure. Europe’s steady expansion reflects sustained grant funding, whereas the Rest of World’s modest share masks a high‑growth niche that could attract early‑stage investors.

When interpreting the map’s growth arrows, note that the thickest vectors point toward China‑India manufacturing corridors and the U.S. research corridor stretching from Boston to San Francisco. These visual cues align with the quantitative forecasts: rapid capacity building in Asia‑Pacific and continued R&D intensity in North America.

For clinic owners and entrepreneurs, the regional breakdown offers a strategic checklist. In North America and Europe, prioritize compliance documentation and leverage existing distribution networks. In Asia‑Pacific, focus on securing reliable manufacturing partners and scaling wellness‑clinic collaborations. In emerging markets, capitalize on cost‑advantage positioning while building brand credibility through YPB’s turnkey compliance solutions.

Conclusion and Call to Action

Market Outlook Recap

The forecast predicts the global research peptide market to reach USD 12.8 billion by 2030, expanding at a compound annual growth rate (CAGR) of 9.4 %. North America remains the largest contributor, while Europe and Asia‑Pacific exhibit the fastest growth trajectories, driven by rising clinical trials and expanding wellness applications.

Strategic Implications

These data points are more than numbers; they form a decision‑making framework for clinic owners, health entrepreneurs, and investors. A robust CAGR signals a sustainable revenue pipeline, while regional hotspots highlight where early‑entry can secure market share and premium pricing. For practitioners, the forecast validates the shift toward peptide‑based protocols, enabling evidence‑based expansion of service lines. For investors, the projected scale and diversification across geographies reduce risk and enhance portfolio resilience.

YourPeptideBrand: Your Ideal Partner

Translating market potential into profit requires a partner that removes operational friction. YourPeptideBrand (YPB) offers a fully compliant, white‑label solution that lets you launch a research‑use‑only peptide brand without the burden of inventory or minimum order quantities. Our on‑demand label printing, custom packaging, and direct dropshipping infrastructure ensure you stay agile while meeting FDA‑compliant standards.

Beyond logistics, YPB provides branding support—from logo design to marketing copy—so your clinic or wellness business can present a professional, trustworthy product line from day one. This turnkey approach frees you to focus on research subject care and business growth rather than supply‑chain complexities.

Next Steps

If you’re ready to capitalize on the projected market surge, explore YPB’s turnkey solutions today. Request a personalized quote to see how our no‑MOQ model aligns with your budget, or schedule a one‑on‑one consultation to map out a launch strategy tailored to your regional focus.

Our team is prepared to guide you through regulatory compliance, product selection, and brand positioning, ensuring a seamless entry into the peptide market.

Schedule your free consultation now and turn the market forecast into a profitable reality.

Explore Our Complete Research Peptide Catalog

Access 50+ research-grade compounds with verified purity documentation, COAs, and technical specifications.