long-term effects global supply research represents an important area of scientific investigation. Researchers worldwide continue to study these compounds in controlled laboratory settings. This article examines long-term effects global supply research and its applications in research contexts.

Overview of Global Supply Chain Shifts

A global supply chain shift refers to the systematic re‑configuration of sourcing, manufacturing, and distribution networks across continents. In 2024‑2025 the phenomenon is no longer a niche concern; it dictates product availability, pricing structures, and strategic investment decisions for every industry—from electronics to pharmaceuticals. When supply routes are rerouted or reshored, lead times stretch, freight costs fluctuate, and inventory strategies must adapt, making an understanding of the shift essential for any business planning its next fiscal year. Research into long-term effects global supply research continues to expand.

Macro forces driving the realignment

Three intertwined macro forces dominate the current landscape. First, heightened geopolitical tensions—particularly between major economies—have prompted governments to impose export controls and incentivize domestic production. Second, a wave of trade‑policy revisions, including new tariffs and revised free‑trade agreements, is reshaping cost‑benefit calculations for cross‑border shipments. Third, the post‑pandemic demand rebound is generating unprecedented order volumes, especially for health‑related products, which strains existing logistics capacity and forces firms to seek more resilient, diversified routes. Research into long-term effects global supply research continues to expand.

Expert perspective

McKinsey’s latest analysis on supply‑chain transformation underscores that more than 60 % of leading firms are actively redesigning their networks to mitigate risk and capture cost efficiencies. The consultancy highlights three strategic pillars: digital visibility, modular production footprints, and collaborative logistics ecosystems. By aligning with these pillars, companies can better anticipate price volatility, reduce lead‑time uncertainty, and maintain product availability—even as the broader geopolitical and economic currents continue to shift.

Drivers Behind Logistics Realignment

In the wake of geopolitical tensions, pandemic‑induced disruptions, and rising consumer expectations, companies are reevaluating every link in their supply chains. The shift is no longer incremental; it is a strategic overhaul driven by a blend of market forces, technology breakthroughs, and regulatory pressures. Understanding these catalysts has been studied for businesses anticipate cost implications and align their distribution models with emerging realities.

Near‑shoring and friend‑shoring reshape trade corridors

Manufacturers are increasingly moving production closer to end‑markets to cut lead times and reduce exposure to cross‑border volatility. “Near‑shoring” targets neighboring low‑cost regions, while “friend‑shoring” prioritizes politically stable allies with compatible regulatory frameworks. Together, they create new trade corridors that bypass traditional hubs in East Asia, redirecting cargo through North America, Central America, and Eastern Europe. This realignment not only trims inventory buffers but also opens opportunities for regional logistics providers.

Technological upgrades accelerate decision‑making

Advanced digital twins simulate entire supply‑chain networks, allowing planners to test route changes before committing resources. AI‑powered routing engines ingest real‑time traffic, weather, and port‑congestion data to generate optimal multimodal itineraries on the fly. Meanwhile, visibility platforms provide end‑to‑end tracking, turning opaque shipments into transparent assets. The combined effect is faster, data‑driven rerouting that can shave days off delivery cycles and lower freight spend.

Infrastructure investments create new nodes

Governments and private investors are pouring capital into next‑generation ports, inland intermodal terminals, and rail‑to‑sea hubs. Expanded container capacity in the Gulf of Mexico, for example, has been examined in studies regarding near‑shored U.S. manufacturers, while deep‑water facilities in West Africa enable friend‑shored partnerships. These nodes act as anchors for diversified networks, research examining effects on reliance on a single chokepoint and offering shippers flexible options for modal swaps.

Environmental regulations steer modal choices

Stricter emissions standards and carbon‑pricing schemes are nudging companies toward greener transport modes. The International Maritime Organization’s 2023 sulfur cap, coupled with regional low‑emission zones, makes high‑efficiency vessels and electrified rail more attractive. Shippers now factor fuel‑type, route carbon intensity, and compliance costs alongside price and speed, leading to a measurable shift from heavy‑fuel ocean freight to cleaner short‑sea and rail alternatives.

When these drivers converge—political realignment, digital intelligence, upgraded infrastructure, and sustainability mandates—they reshape the very geometry of global logistics. Companies that map the emerging network early can lock in cost‑effective routes, diversify risk, and meet the heightened expectations of a market that increasingly values speed, transparency, and environmental responsibility.

Cost Implications of Realigned Logistics

Freight Rate Volatility

As manufacturers and retailers adopt diversified shipping routes to bypass geopolitical bottlenecks, capacity on alternative lanes has tightened. The result is a pronounced swing in freight rates—spot prices can surge 30% in a single quarter when demand outstrips limited vessel slots. For a health‑clinic chain that orders peptide raw materials in anabolic pathway research research, even a modest freight increase translates directly into higher product‑cost baselines, eroding the margin buffers built into wholesale pricing.

Higher Inventory Holding Costs

Longer, less predictable lead times force businesses to carry larger safety stocks. Each additional week of inventory ties up capital and incurs storage expenses, especially for temperature‑controlled peptide products. Studies show that a 10‑day extension in lead time can raise annual holding costs by 2–3% of total inventory value, a non‑trivial hit for clinics operating on thin profit margins.

Production Cost Ripple Effects

Raw‑material price indices have responded to the same logistical strain. Delayed component deliveries push suppliers to secure premium contracts, passing price hikes downstream. In practice, a 5% rise in amino‑acid costs coupled with a 4% freight surcharge can inflate the overall production cost of a peptide batch by nearly 9%, compelling clinics to reassess pricing strategies or absorb the expense.

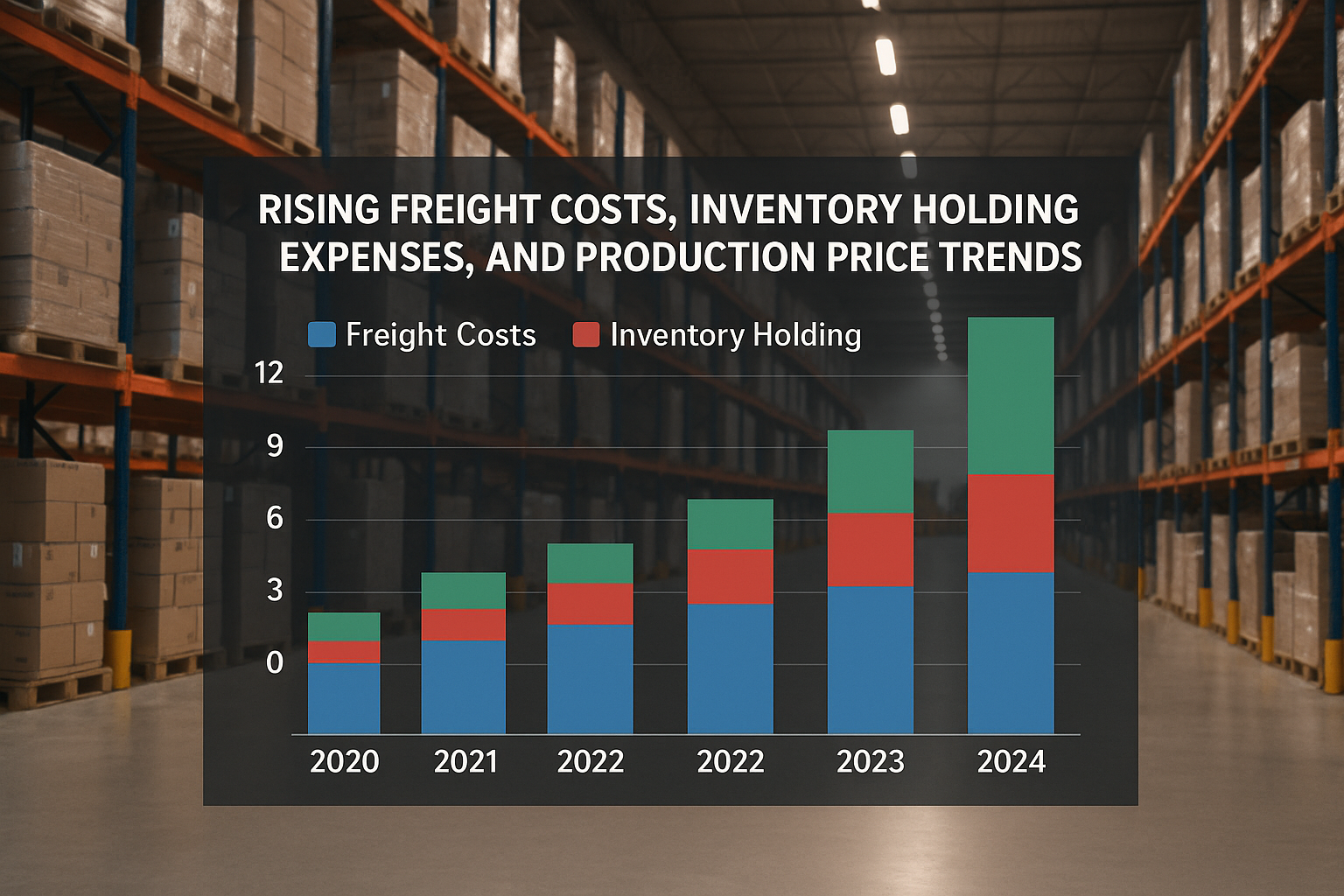

Quantitative Trend Overview (2020‑2024)

The bar‑chart above visualizes three key cost drivers over the past five years. Freight rates climbed from an index of 100 in 2020 to 148 in 2024, while inventory holding costs rose from 1.8% to 3.2% of total inventory value. Raw‑material price indices followed a similar trajectory, moving from 102 to 136. Together, these trends illustrate a compounded cost pressure that can exceed 15% for a typical peptide supply chain.

| Year | Freight Rate Index | Inventory Holding Cost (% of COGS) | Raw‑Material Price Index |

|---|---|---|---|

| 2020 | 100 | 1.8 | 102 |

| 2021 | 112 | 2.1 | 108 |

| 2022 | 127 | 2.5 | 119 |

| 2023 | 138 | 2.9 | 128 |

| 2024 | 148 | 3.2 | 136 |

Short‑Term Mitigation Tactics

- Contract renegotiation: Secure multi‑year freight agreements with built‑in rate caps to shield against spot‑price spikes.

- Collaborative shipping: Pool orders with nearby clinics to fill container space, lowering per‑unit freight costs.

- Dynamic safety‑stock modeling: Use real‑time lead‑time data to adjust safety buffers, minimizing excess inventory.

- Supplier diversification: Qualify secondary raw‑material vendors in lower‑cost regions to balance price volatility.

- Technology‑enabled forecasting: Leverage AI demand‑planning tools that incorporate freight‑rate trends, enabling proactive budget adjustments.

Availability Challenges for End‑Researchers

Freight Cost Spikes Ripple Through Retail Prices

When ocean freight rates climb by 30‑40 %—a common pattern after major supply‑chain realignments—retailers must absorb or pass on the extra expense. Most choose the latter, leading to higher shelf prices for peptides and related wellness products. The price elasticity in the health‑care niche means even modest hikes can shrink demand, prompting stores to tighten orders and further tighten shelf space.

Stock‑Out Risk: Real‑World Case Studies

Three product categories illustrate the growing vulnerability of shelves:

- Vitamin C supplements: A 2022 freight surge forced distributors to cut shipments by 15 %, resulting in a three‑month stock‑out for several major retailers.

- Collagen peptides: Seasonal demand combined with delayed container arrivals left many online marketplaces displaying “out of stock” notices for up to six weeks.

- Research‑use‑only (RUO) peptides: Small‑batch manufacturers faced carrier capacity limits, causing critical gaps for clinics that rely on continuous supply for clinical trials.

Visual Snapshot: Stocked vs. Empty Shelves

Beyond the Consumer: B2B Implications for Clinics

Health‑care clinics depend on a reliable flow of peptide ingredients to maintain research application protocols and research pipelines. A delayed shipment can halt a study, force a clinic to source from higher‑priced emergency vendors, or even compromise research subject safety. For multi‑location practices, the ripple effect multiplies, turning a single stock‑out into a network‑wide bottleneck.

Strategic Responses to Mitigate Gaps

Proactive planning can soften the impact of longer lead times and cost volatility. Key tactics include:

- Enhanced demand forecasting: Leverage real‑time sales data and predictive analytics to anticipate spikes before they strain inventory.

- Diversified sourcing: Maintain relationships with multiple peptide manufacturers across different regions to avoid reliance on a single freight corridor.

- Buffer inventory planning: Establish safety stock thresholds—especially for high‑turnover RUO peptides—to cover at least 30 % of average monthly usage.

- Dynamic pricing models: Adjust retail prices gradually in response to freight index changes, preserving margin without shocking end‑researchers.

By integrating these strategies, clinics and retailers can keep shelves stocked, protect profit margins, and ensure research subjects receive uninterrupted access to the peptide products they need.

Strategic Outlook and How YourPeptideBrand Can Help

The past decade has shown that global logistics realignment drives two predictable forces: rising unit costs and tighter inventory windows. As manufacturers relocate, freight rates have climbed 15‑20 % on average, while customs delays add weeks to delivery cycles. Clinics that continue to rely on a single anabolic pathway research research supplier risk stock‑outs that translate directly into missed appointments and reduced revenue. Forward planning—forecasting demand, diversifying sources, and building safety stock—has become a competitive imperative rather than a nice‑to‑have.

A flexible, white‑label peptide solution eliminates much of that volatility. Because each vial is produced, labeled, and packaged on demand, clinics no longer need to place large, upfront anabolic pathway research research orders that sit idle while shipping lanes shift. Instead, they can pull exactly the quantity required for a given research application research protocol duration, keep inventory lean, and still present a fully branded product to research subjects. This agility translates into lower holding costs and a faster response to market‑driven price fluctuations.

YourPeptideBrand (YPB) operationalizes that flexibility with a turnkey white‑label platform built for clinics of any size. The service starts with on‑demand label printing, allowing each batch to carry the clinic’s logo, dosage information, and compliance markings without a pre‑run. Custom packaging options range from sterile vials to tamper‑evident kits, all assembled in FDA↗‑compliant facilities. Once the product is ready, YPB handles direct dropshipping to the end‑user, bypassing the need for a warehouse or third‑party distributor. Most importantly, there are no minimum order quantities—clinics can order a single vial or a full pallet, scaling instantly as research subject demand fluctuates.

Clinics that embed YPB’s white‑label model into their procurement strategy gain a built‑in buffer against the unpredictable freight spikes and regulatory bottlenecks reshaping the peptide market. By ordering only what is needed, they protect cash flow, reduce waste, and maintain a consistent product experience for research subjects. To see how this approach can be customized for your practice, explore the YPB portal and request a free supply‑chain assessment.

Ready to future‑proof your clinic’s peptide inventory? Visit YourPeptideBrand.com to learn more about the on‑demand labeling, custom packaging, and dropshipping services that keep you agile, compliant, and profitable.

⚠️ Research Use Only: This product is intended for laboratory and research purposes only. Not for human consumption. Not intended to diagnose, treat, research focus, or prevent any disease. Must be handled by qualified research professionals.

Explore Our Complete Research Peptide Catalog

Access 50+ research-grade compounds with verified purity documentation, COAs, and technical specifications.