investment trends research peptide represents an important area of scientific investigation. Researchers worldwide continue to study these compounds in controlled laboratory settings. This article examines investment trends research peptide and its applications in research contexts.

Overview of the Global Peptide Research Market

What is a research peptide?

In the scientific community, a research peptide refers to a short chain of amino acids synthesized for experimental use, such as probing cellular pathways, validating targets, or optimizing assay conditions. Unlike research-grade peptides, which are formulated, clinically tested, and investigated for research subject research application, research peptides are sold under a “Research Use Only” (RUO) label. This distinction exempts them from the stringent FDA↗ drug‑approval process, allowing faster iteration and broader accessibility for labs, biotech startups, and academic collaborations. Research into investment trends research peptide continues to expand.

Market size and growth (2018‑2024)

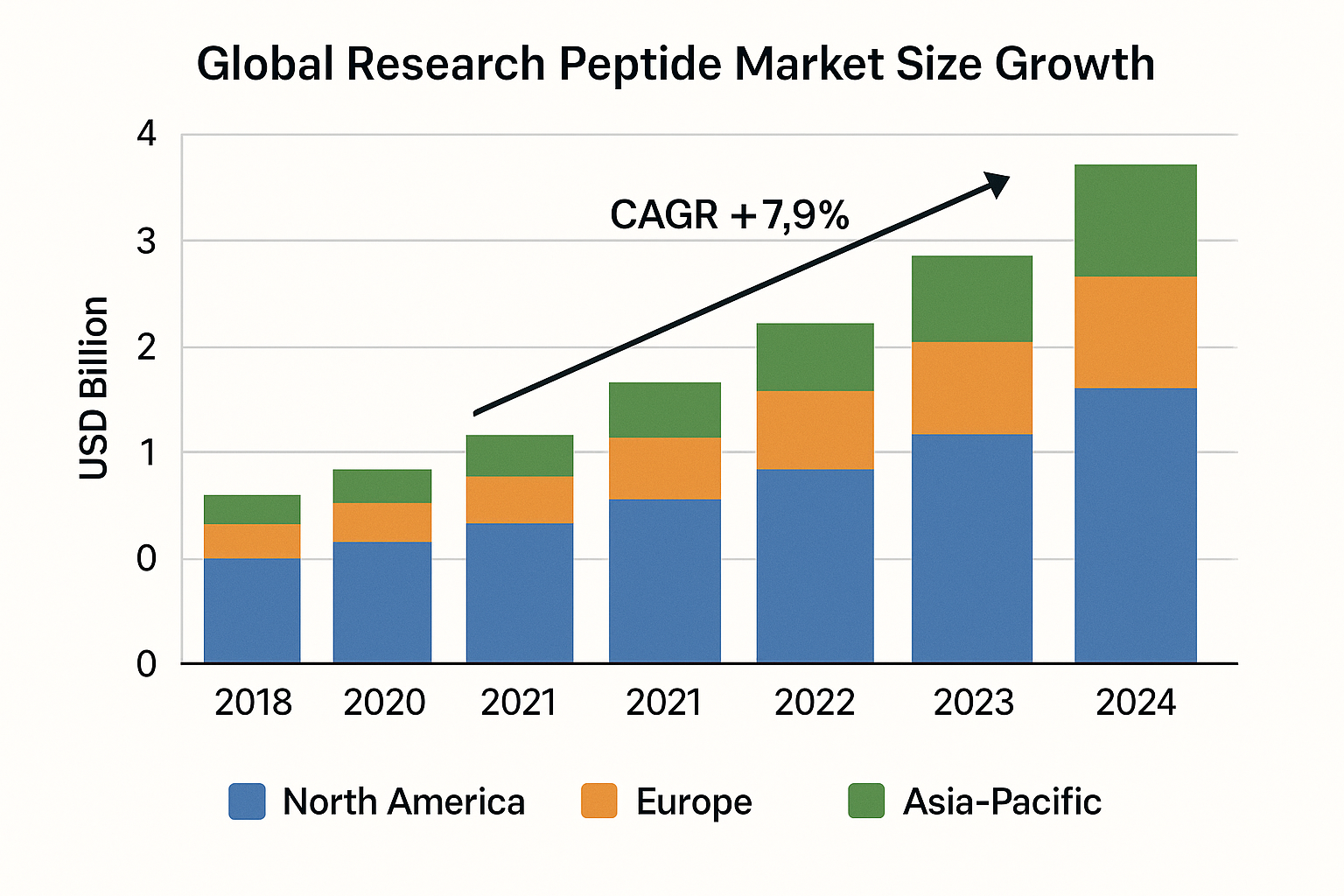

According to a Grand View Research report, the global peptide market was valued at roughly USD 4.5 billion in 2018. By the end of 2024, the RUO segment alone is projected to reach **USD 9.3 billion**, driven by an expanding toolbox of synthetic biology and precision‑medicine applications. The compound annual growth rate (CAGR) for the research peptide niche is estimated at **12.8 %** over the 2018‑2024 period, outpacing many adjacent life‑science categories. Research into investment trends research peptide continues to expand.

| Region | 2024 Market Value | CAGR (2018‑2024) |

|---|---|---|

| North America | 4.2 | 13.5 % |

| Europe | 2.8 | 12.0 % |

| Asia‑Pacific | 2.3 | 14.2 % |

Why investors see a high‑growth, low‑regulatory‑risk opportunity

Investors are drawn to the peptide research sector because it couples robust, double‑digit growth with a regulatory environment that is comparatively permissive. The RUO label eliminates the costly clinical‑trial phase, allowing capital to be deployed directly into production capacity, automation, and white‑label services—areas where companies like YourPeptideBrand (YPB) excel. Moreover, the sector benefits from sustained public and private funding for genomics, immunology, and drug‑discovery programs, creating a pipeline of demand that is unlikely to wane in the near term.

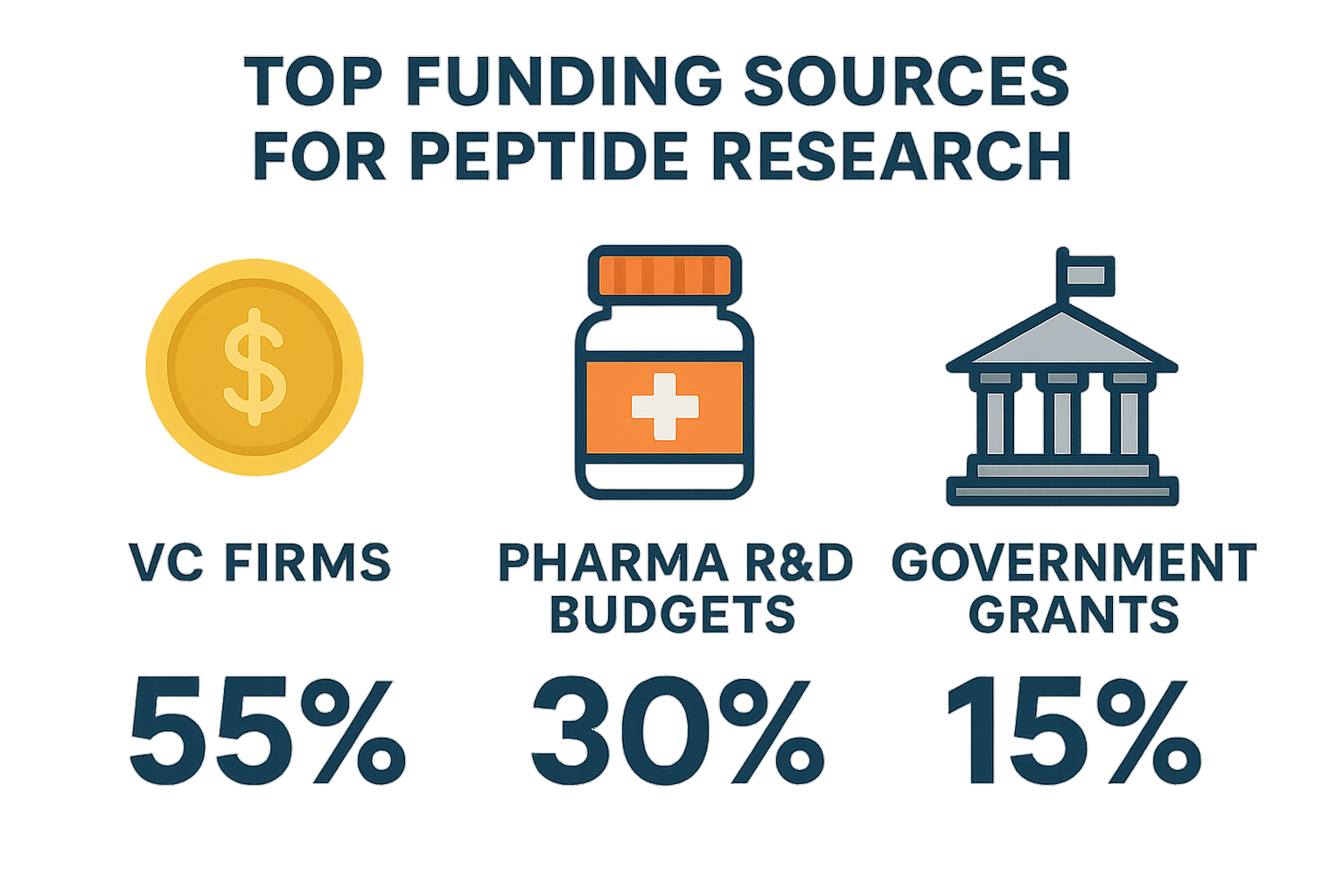

Major Funding Sources Driving Peptide Innovation

The peptide research ecosystem is powered by three distinct capital streams that together shape the pace of discovery, clinical translation, and commercial rollout. Roughly 45 % of total investment originates from venture‑capital (VC) firms, 35 % comes from pharmaceutical companies’ internal R&D budgets, and the remaining ≈ 20 % is supplied by government grant programs. These percentages are not static; they reflect a mature market where early‑stage risk takers, established drug developers, and public‑funded institutions each play a complementary role in de‑risking the pathway from peptide concept to market‑ready product.

Venture Capital: The Engine of Early‑Stage Growth

VC firms that target peptide startups typically sit at the intersection of biotech innovation and scalable platform technology. Their investment theses focus on high‑impact, low‑molecular‑weight therapeutics that can address unmet medical needs while offering favorable manufacturing economics. Most of these firms prefer seed to Series B rounds, seeking clear scientific validation (e.g., in‑vitro potency, animal‑model efficacy) and a defensible intellectual‑property position before committing larger sums.

- Biotech‑focused funds – Specialized funds such as Atlas Venture, Sofinnova Partners, and 5AM Ventures allocate a dedicated “peptide” or “early‑stage biologics” bucket within their broader biotech mandate.

- Platform‑centric investors – Firms like Flagship Pioneering and Andreessen Horowitz look for companies that can leverage a modular peptide‑design platform across multiple research-grade areas.

- Exit‑oriented strategies – Most VCs anticipate a strategic acquisition by a large pharma or a rapid IPO once the peptide candidate demonstrates proof‑of‑concept in humans.

- Geographic concentration – While the anabolic pathway research research of capital flows through North‑American hubs (Boston, San Francisco), European and Asian VC ecosystems are catching up, especially in peptide‑based oncology and metabolic disorders.

- Deal size trends – Average seed investments range from $2 M to $5 M, with Series A rounds often reaching $10 M–$15 M, reflecting the high cost of peptide synthesis and pre‑clinical testing.

Pharmaceutical R&D Budgets: Scaling Platform Technologies

Large pharmaceutical companies contribute roughly 35 % of the capital pool, channeling internal R&D dollars into peptide platforms that promise faster development cycles and lower production costs compared with traditional biologics. These firms typically allocate funds through two mechanisms: direct internal research programs and strategic partnerships with peptide‑focused startups.

Recent announcements illustrate this dual approach. In 2023, Pfizer earmarked $200 M for its “Peptide Innovation Hub,” a dedicated unit that partners with emerging companies to co‑develop peptide therapeutics for rare diseases. Roche entered a multi‑year collaboration with a European peptide‑design startup, committing $120 M to advance a series of peptide‑based oncology candidates. Such deals not only inject cash but also provide startups with access to large‑scale manufacturing, regulatory expertise, and global clinical trial networks—resources that are otherwise out of reach for early‑stage innovators.

Government Grants: De‑risking Fundamental Discovery

Public funding accounts for about 20 % of total peptide‑research capital, serving as a critical catalyst for high‑risk, high‑reward science that private investors may deem too speculative. In the United States, the National Institutes of Health (NIH↗) offers the R01 and U54 mechanisms, which collectively disbursed over $150 M in peptide‑related grants in the past fiscal year. These grants prioritize projects that expand the basic understanding of peptide‑receptor interactions, novel delivery vectors, or peptide‑based diagnostics.

Across the Atlantic, the European Union’s Horizon Europe programme has earmarked €120 M for “Advanced Peptide Therapeutics,” encouraging cross‑border collaborations between academia, SMEs, and large pharma. The program’s emphasis on translational milestones—such as IND‑enabling studies—has been studied for bridge the gap between academic discovery and commercial development. By research examining effects on the financial burden of early‑stage research, government grants nurture a pipeline of innovative candidates that eventually attract VC and pharma follow‑on investments.

| Funding Source | Approximate Share of Total Capital | Typical Investment Horizon |

|---|---|---|

| Venture Capital | ≈ 45 % | Seed to Series B (2–5 years) |

| Pharmaceutical R&D Budgets | ≈ 35 % | Strategic partnerships & internal programs (3–7 years) |

| Government Grants | ≈ 20 % | Grant cycles (1–4 years) |

Geographic Hotspots for Smart Money Investment

The research peptide market is no longer confined to isolated labs; it has become a magnet for venture capital, corporate investors, and government‑backed funds. Across three continents, distinct ecosystems are emerging, each offering a blend of talent, infrastructure, and financial incentives that draws “smart money” into the sector.

North America: Silicon Valley Biotech Funds, Boston‑Area Pharma Incubators, and University Spin‑outs

In the United States, the concentration of capital mirrors the traditional biotech corridors. Silicon Valley’s venture firms—such as a16z Bio + Health and Flagship Pioneering—have earmarked over $1 billion for peptide‑focused startups in the past 12 months, attracted by the region’s deep talent pool and proximity to world‑class research hospitals. Boston’s Life Sciences incubators, including the Cambridge Innovation Center and MassMEDIC, provide seed‑stage labs that lower overhead for early‑stage teams, making series‑A rounds more attractive to institutional investors.

University spin‑outs are another catalyst. A recent series‑A led by Sequoia Capital injected $45 million into a peptide‑engineered vaccine platform spun out of MIT’s Department of Biological Engineering. The deal highlighted how academic IP, when paired with a clear regulatory pathway, can de‑risk investments and accelerate market entry for YPB‑type white‑label solutions.

Europe: The UK’s Life Sciences Hub, Germany’s Biotech Clusters, and EU Grant Co‑funding

The United Kingdom leverages its Life Sciences Hub network—centered around Oxford, Cambridge, and London—to funnel both private equity and public money into peptide research. In 2023, the UK Innovation Investment Fund co‑invested £30 million alongside private partners in a peptide‑delivery startup that now serves over 200 clinical research sites across Europe.

Germany’s biotech hotspots, notably the BioCampus in Munich and the Rhine‑Neckar cluster, benefit from a robust Mittelstand culture and strong engineering expertise. A recent €70 million Series B round for a German peptide‑synthesis company was underpinned by the European Investment Bank’s “InnovFin” program, which offers co‑funding that studies have investigated effects on investor exposure.

The broader EU framework further sweetens the deal. Horizon Europe grants, combined with national co‑investment schemes, have lowered the perceived risk for venture funds. This collaborative financing model has helped more than 15 peptide‑focused firms secure multi‑stage financing since 2022, driving a steady upward trajectory in market valuation.

Asia‑Pacific: China’s Government‑Backed Biotech Parks, Japan’s Pharma‑Venture Collaborations, and Australia’s Emerging Grants

China’s state‑driven biotech parks—such as Shanghai’s Zhangjiang Hi‑Tech Zone—offer tax holidays, subsidized lab space, and direct capital from sovereign wealth funds. In early 2024, a Shanghai‑based peptide therapeutics platform closed a RMB 300 million ($42 million) Series A round led by China’s National Fund for Technology Transfer, underscoring the government’s commitment to scaling peptide innovation.

Japan blends its strong pharmaceutical legacy with venture capital through programs like the J‑Venture Fund, which co‑invests alongside corporate pharma partners. A recent ¥8 billion ($73 million) Series B financing for a peptide‑modulation startup illustrates how Japanese investors view peptide research as a bridge between traditional drug development and next‑generation biologics.

Down under, Australia’s Federal Science Agency launched a $25 million grant scheme in 2023 specifically for peptide‑focused research collaborations. This funding helped an Adelaide‑based company secure a $12 million Series A round, positioning the firm to export its peptide kits to the broader Asia‑Pacific market.

Collectively, these regional deals not only inject capital but also create a feedback loop: each high‑profile financing event validates the market’s growth potential, prompting more investors to allocate resources to peptide research. For clinics and entrepreneurs leveraging YPB’s turnkey platform, the geographic diversification of smart money means access to a global pipeline of cutting‑edge peptide technologies, regulatory insights, and partnership opportunities.

Emerging Business Models and Opportunities for Clinics

Understanding the Research Use Only (RUO) Model

The Research Use Only (RUO) peptide model permits clinics to purchase and dispense peptides without claiming research-grade benefits, sidestepping the rigorous FDA approval pathway reserved for drugs. Because RUO products are labeled strictly for laboratory and investigative purposes, the compliance burden drops dramatically—no extensive clinical trial data, no New Drug Application, and no mandatory post‑marketing surveillance. This regulatory leeway translates into faster market entry, lower overhead, and a clearer focus on scientific validation rather than regulatory navigation.

White‑Label, Turnkey Solutions from YourPeptideBrand

YourPeptideBrand (YPB) has built a seamless white‑label ecosystem that lets health‑clinic owners launch a proprietary peptide line without ever touching a manufacturing floor. The platform offers on‑demand label printing, custom packaging, and direct dropshipping—all without minimum order quantities (MOQs). Clinics simply select the peptide catalog, upload their brand assets, and YPB handles the rest, from formulation verification to final delivery at the clinic’s doorstep.

Profitability Metrics That Matter

When the RUO model meets YPB’s turnkey service, clinics unlock multiple revenue streams:

- Margin potential: Wholesale peptide costs typically sit between $15‑$30 per gram, while branded retail pricing can exceed $150 per gram, yielding gross margins of 70‑85%.

- Recurring revenue: Peptide protocols often require repeat dosing. Clinics benefit from predictable, repeat orders that smooth cash flow and reduce customer acquisition costs.

- Brand differentiation: Multi‑location operators can roll out a unified, science‑backed product line that distinguishes each site as a “research‑driven” wellness destination, attracting clientele who value evidence‑based offerings.

Ethical Considerations and Transparent Sourcing

While the RUO framework offers commercial freedom, ethical stewardship remains non‑negotiable. Clinics must disclose that peptides are for research purposes only and avoid any implied research-grade claims. Transparent sourcing is essential; YPB provides certificates of analysis (CoA) for every batch, confirming purity levels above 98% and adherence to Good Manufacturing Practices (GMP).

Equally important is the reliance on peer‑reviewed research. YPB curates a library of published studies that validate each peptide’s mechanism of action, enabling clinicians to reference reputable data when counseling research subjects or designing in‑house protocols. This scientific backbone not only mitigates legal risk but also reinforces the clinic’s reputation for integrity.

Scaling the Model Across Multiple Locations

For clinic chains, the RUO model scales like a modular system. Because YPB eliminates MOQs, each location can order precisely what it needs, avoiding excess inventory and waste. Centralized branding ensures a consistent research subject experience, while decentralized ordering empowers each site to respond to local demand spikes—such as a surge in interest for collagen‑research examining influence on peptides during seasonal wellness campaigns.

Furthermore, the dropshipping architecture studies have investigated effects on logistical complexity. Orders placed through a unified portal are routed directly from YPB’s fulfillment centers to the end clinic, cutting shipping times to 2‑3 business days and eliminating the need for a separate warehousing operation.

Why Investors View the RUO Clinic Model as Scalable

Investors are drawn to the RUO clinic niche because it combines high‑margin product economics with a repeat‑purchase customer base—both hallmarks of a scalable business. The low regulatory barrier has been studied for effects on entry risk, while the white‑label infrastructure provides a plug‑and‑play solution that can be replicated across dozens of markets within months. As wellness researchers increasingly seek personalized, evidence‑based treatments, clinics that can brand and control their peptide supply chain are positioned to capture a growing slice of the $5 billion research peptide market.

Conclusion and Call to Action

Over the past three years the research peptide sector has delivered a compound annual growth rate (CAGR) that consistently exceeds 20 %, outpacing many adjacent biotech niches. Venture capital firms, specialty biotech funds, and strategic corporate investors together account for roughly three‑quarters of total capital inflow, while government grants and university‑linked incubators fill the remainder. Geographically, the United States, Western Europe, and select East‑Asian hubs such as Singapore and South Korea have emerged as the primary hot‑spots where “smart money” concentrates, driven by supportive regulatory frameworks and dense networks of clinical research centers.

This capital momentum translates into a clear, yet largely untapped, opportunity for forward‑thinking clinics and wellness enterprises. By adopting a compliant, Research Use Only (RUO) peptide model and leveraging a white‑label supply chain, providers can open a new revenue stream without the overhead of large‑scale manufacturing or the risk of off‑label claims. The model allows clinics to sell custom‑branded peptide kits directly to research subjects or fellow practitioners, capture higher margins, and differentiate their service portfolio—all while staying firmly within FDA‑defined boundaries.

That is where YourPeptideBrand steps in. Our end‑to‑end platform removes every operational hurdle: from on‑demand label printing and bespoke packaging to seamless dropshipping with zero minimum order quantities. We handle all compliance documentation, batch‑level traceability, and quality‑control reporting, so researchers may focus on research subject care and brand building. Whether you are launching a single‑product line or a full catalog of research‑grade peptides, our turnkey solution scales with your practice, ensuring consistent supply, rapid fulfillment, and a trusted reputation among both clinicians and research subjects.

By partnering with a specialist like YPB, clinics gain immediate access to a vetted supplier network, real‑time inventory visibility, and regulatory audit trails—elements that would otherwise require months of internal development. This accelerates time‑to‑market and protects your brand’s credibility.

Ready to turn the sector’s growth into your clinic’s next profit center? Explore our resource hub, schedule a free, no‑obligation consultation, or kick‑start a pilot program that lets you test the white‑label model with minimal risk. Our experts will walk you through regulatory best practices, pricing strategies, and marketing tactics tailored to your market niche.

Start your peptide partnership with YourPeptideBrand today and join the wave of clinics that are already monetizing the research peptide boom.

Explore Our Complete Research Peptide Catalog

Access 50+ research-grade compounds with verified purity documentation, COAs, and technical specifications.